回归图¶

[1]:

%matplotlib inline

[2]:

from statsmodels.compat import lzip

import numpy as np

import matplotlib.pyplot as plt

import statsmodels.api as sm

from statsmodels.formula.api import ols

plt.rc("figure", figsize=(16, 8))

plt.rc("font", size=14)

邓肯的声望数据集¶

加载数据¶

我们可以使用一个实用程序函数来加载任何来自 Rdatasets 包的 R 数据集。

[3]:

prestige = sm.datasets.get_rdataset("Duncan", "carData", cache=True).data

[4]:

prestige.head()

[4]:

| 类型 | 收入 | 教育 | 声望 | |

|---|---|---|---|---|

| 行名 | ||||

| 会计 | 教授 | 62 | 86 | 82 |

| 飞行员 | 教授 | 72 | 76 | 83 |

| 建筑师 | 教授 | 75 | 92 | 90 |

| 作者 | 教授 | 55 | 90 | 76 |

| 化学家 | 教授 | 64 | 86 | 90 |

[5]:

prestige_model = ols("prestige ~ income + education", data=prestige).fit()

[6]:

print(prestige_model.summary())

OLS Regression Results

==============================================================================

Dep. Variable: prestige R-squared: 0.828

Model: OLS Adj. R-squared: 0.820

Method: Least Squares F-statistic: 101.2

Date: Thu, 03 Oct 2024 Prob (F-statistic): 8.65e-17

Time: 15:58:25 Log-Likelihood: -178.98

No. Observations: 45 AIC: 364.0

Df Residuals: 42 BIC: 369.4

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -6.0647 4.272 -1.420 0.163 -14.686 2.556

income 0.5987 0.120 5.003 0.000 0.357 0.840

education 0.5458 0.098 5.555 0.000 0.348 0.744

==============================================================================

Omnibus: 1.279 Durbin-Watson: 1.458

Prob(Omnibus): 0.528 Jarque-Bera (JB): 0.520

Skew: 0.155 Prob(JB): 0.771

Kurtosis: 3.426 Cond. No. 163.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

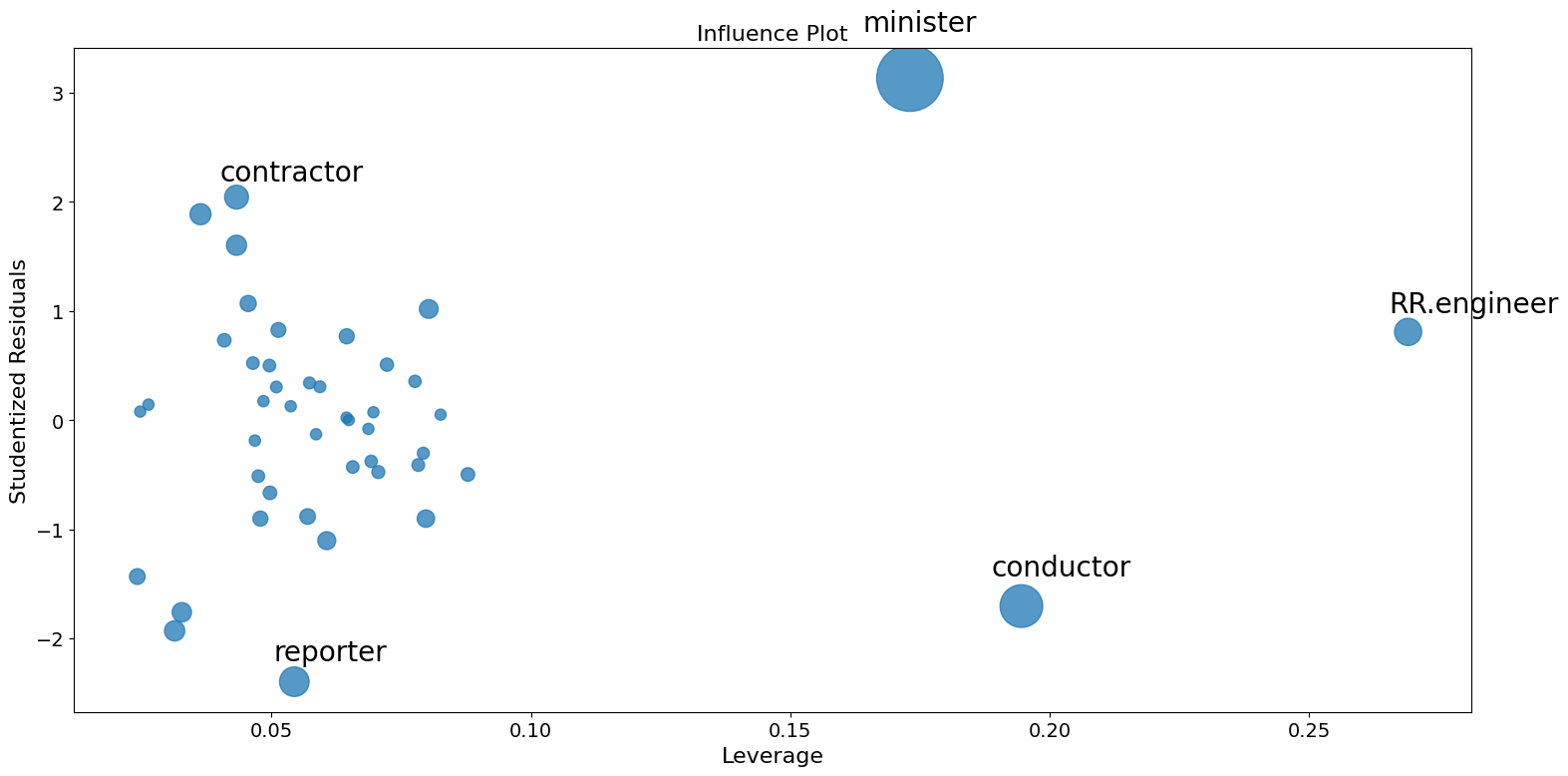

影响图¶

影响图显示了(外部)学生化残差与每个观测值的杠杆率,该杠杆率由帽子矩阵测量。

外部学生化残差是按其标准差缩放的残差,其中

其中

\(n\) 是观测值的数目,\(p\) 是回归变量的数目。 \(h_{ii}\) 是帽子矩阵的第 \(i\) 个对角元素

每个点的影响可以通过 criterion 关键字参数可视化。选项包括 Cook 距离和 DFFITS,这是影响的两种度量。

[7]:

fig = sm.graphics.influence_plot(prestige_model, criterion="cooks")

fig.tight_layout(pad=1.0)

正如你所看到的,有一些令人担忧的观察结果。承包商和记者的杠杆率都很低,但残差很大。RR.engineer 的残差很小,杠杆率很大。指挥家和牧师既有高杠杆率又有大残差,因此影响很大。

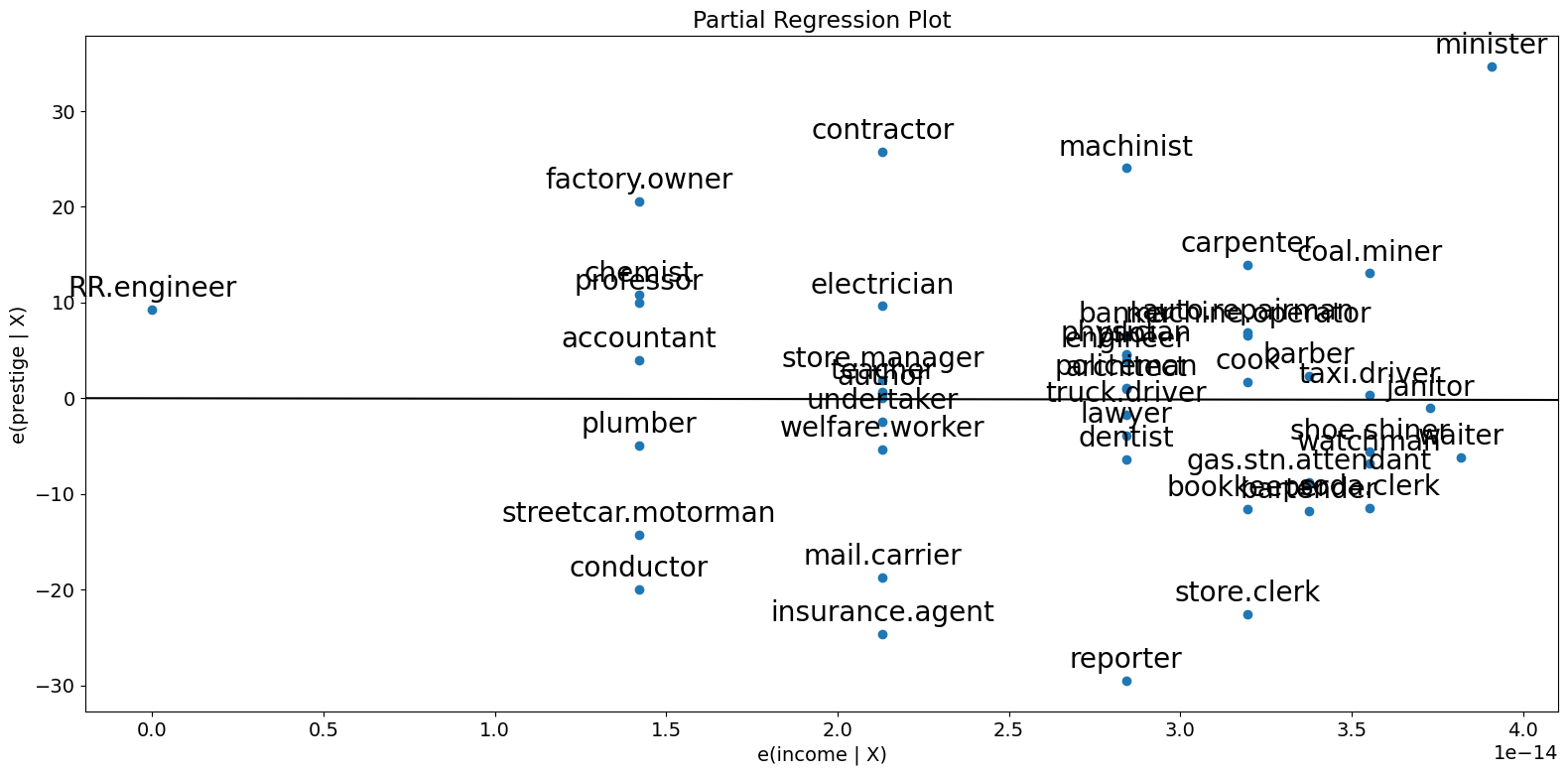

偏回归图 (邓肯)¶

由于我们正在进行多元回归,我们不能仅仅查看单个双变量图来辨别关系。相反,我们想要查看因变量与自变量在其他自变量条件下的关系。我们可以通过使用偏回归图来做到这一点,也称为添加变量图。

在偏回归图中,为了辨别响应变量与第 \(k\) 个变量的关系,我们通过回归响应变量与除 \(X_k\) 以外的自变量来计算残差。我们可以用 \(X_{\sim k}\) 表示它。然后,我们通过回归 \(X_k\) 与 \(X_{\sim k}\) 来计算残差。偏回归图是前者与后者残差的图。

该图值得注意的点是,拟合线的斜率为 \(\beta_k\),截距为零。该图的残差与完整 \(X\) 的原始模型的最小二乘拟合的残差相同。你可以很容易地辨别出各个数据值对系数估计的影响。如果 obs_labels 为 True,则这些点将用其观测值标签进行标注。你还可以看到对基本假设的违反,例如同方差性和线性性。

[8]:

fig = sm.graphics.plot_partregress(

"prestige", "income", ["income", "education"], data=prestige

)

fig.tight_layout(pad=1.0)

[9]:

fig = sm.graphics.plot_partregress("prestige", "income", ["education"], data=prestige)

fig.tight_layout(pad=1.0)

正如你所看到的,偏回归图证实了指挥家、牧师和 RR.engineer 对收入与声望之间偏关系的影响。这些案例大大降低了收入对声望的影响。删除这些案例证实了这一点。

[10]:

subset = ~prestige.index.isin(["conductor", "RR.engineer", "minister"])

prestige_model2 = ols(

"prestige ~ income + education", data=prestige, subset=subset

).fit()

print(prestige_model2.summary())

OLS Regression Results

==============================================================================

Dep. Variable: prestige R-squared: 0.876

Model: OLS Adj. R-squared: 0.870

Method: Least Squares F-statistic: 138.1

Date: Thu, 03 Oct 2024 Prob (F-statistic): 2.02e-18

Time: 15:58:28 Log-Likelihood: -160.59

No. Observations: 42 AIC: 327.2

Df Residuals: 39 BIC: 332.4

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -6.3174 3.680 -1.717 0.094 -13.760 1.125

income 0.9307 0.154 6.053 0.000 0.620 1.242

education 0.2846 0.121 2.345 0.024 0.039 0.530

==============================================================================

Omnibus: 3.811 Durbin-Watson: 1.468

Prob(Omnibus): 0.149 Jarque-Bera (JB): 2.802

Skew: -0.614 Prob(JB): 0.246

Kurtosis: 3.303 Cond. No. 158.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

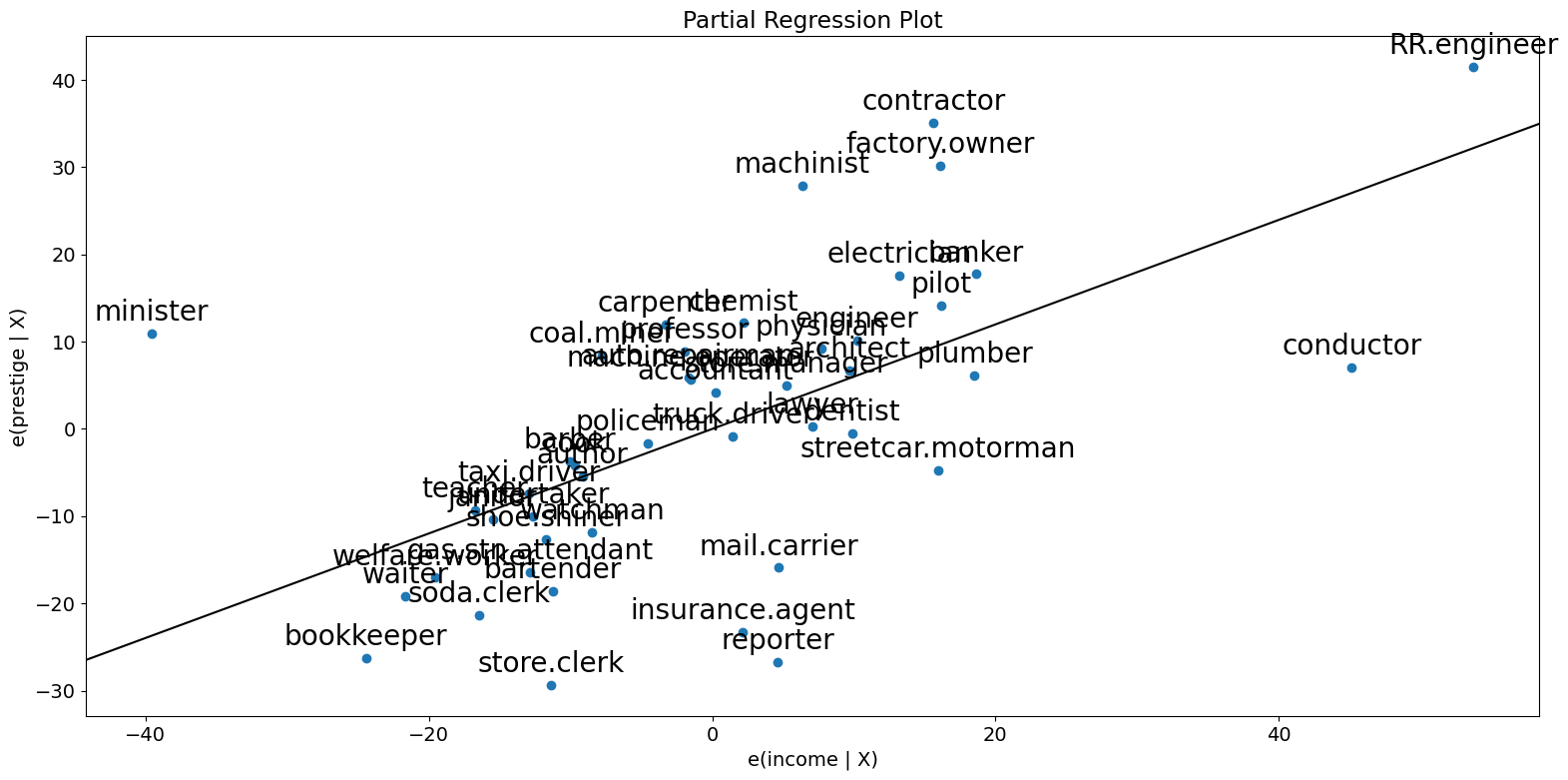

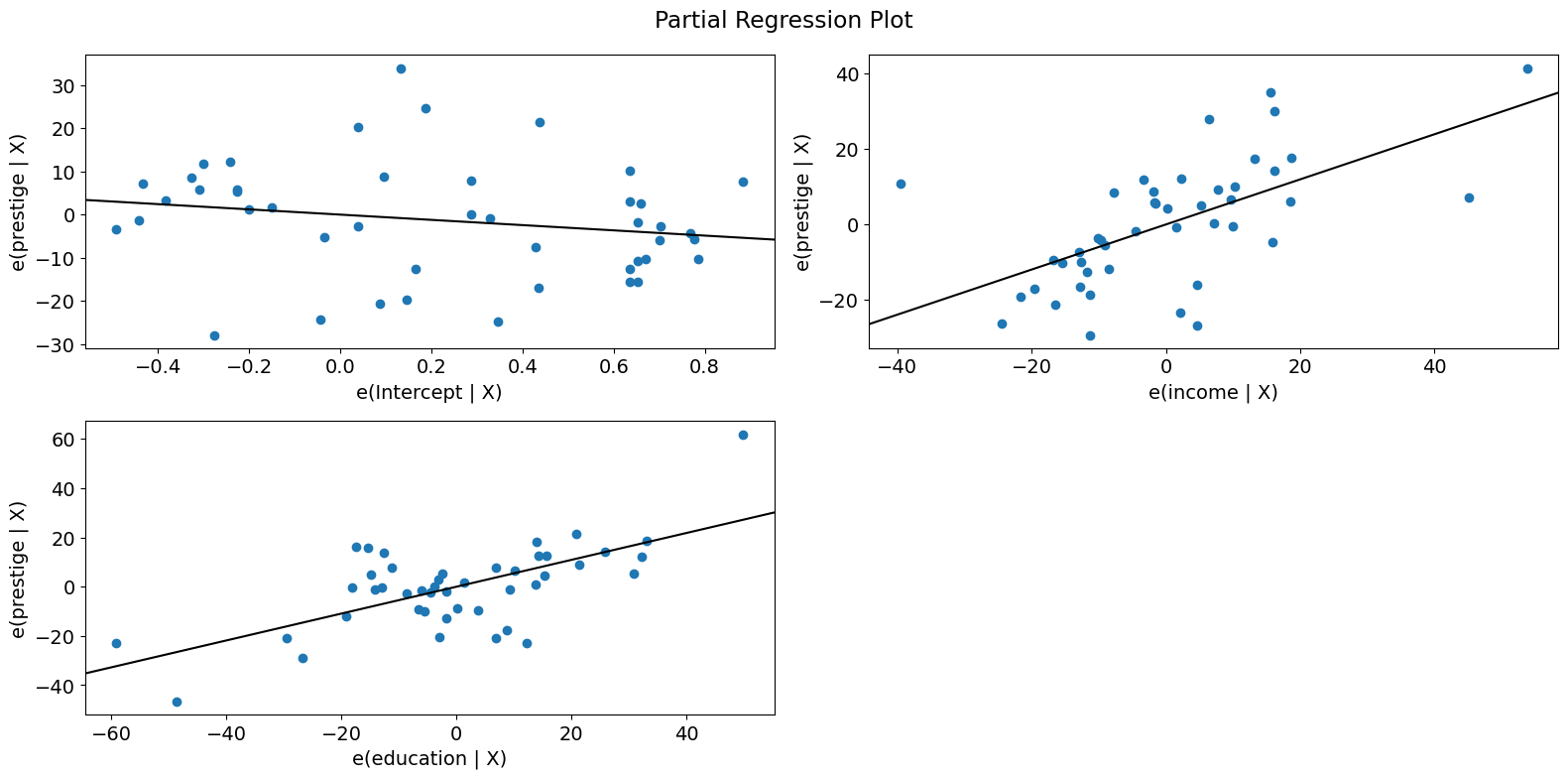

要快速检查所有回归变量,你可以使用 plot_partregress_grid。这些图不会标注点,但你可以使用它们来识别问题,然后使用 plot_partregress 获取更多信息。

[11]:

fig = sm.graphics.plot_partregress_grid(prestige_model)

fig.tight_layout(pad=1.0)

成分-成分加残差 (CCPR) 图¶

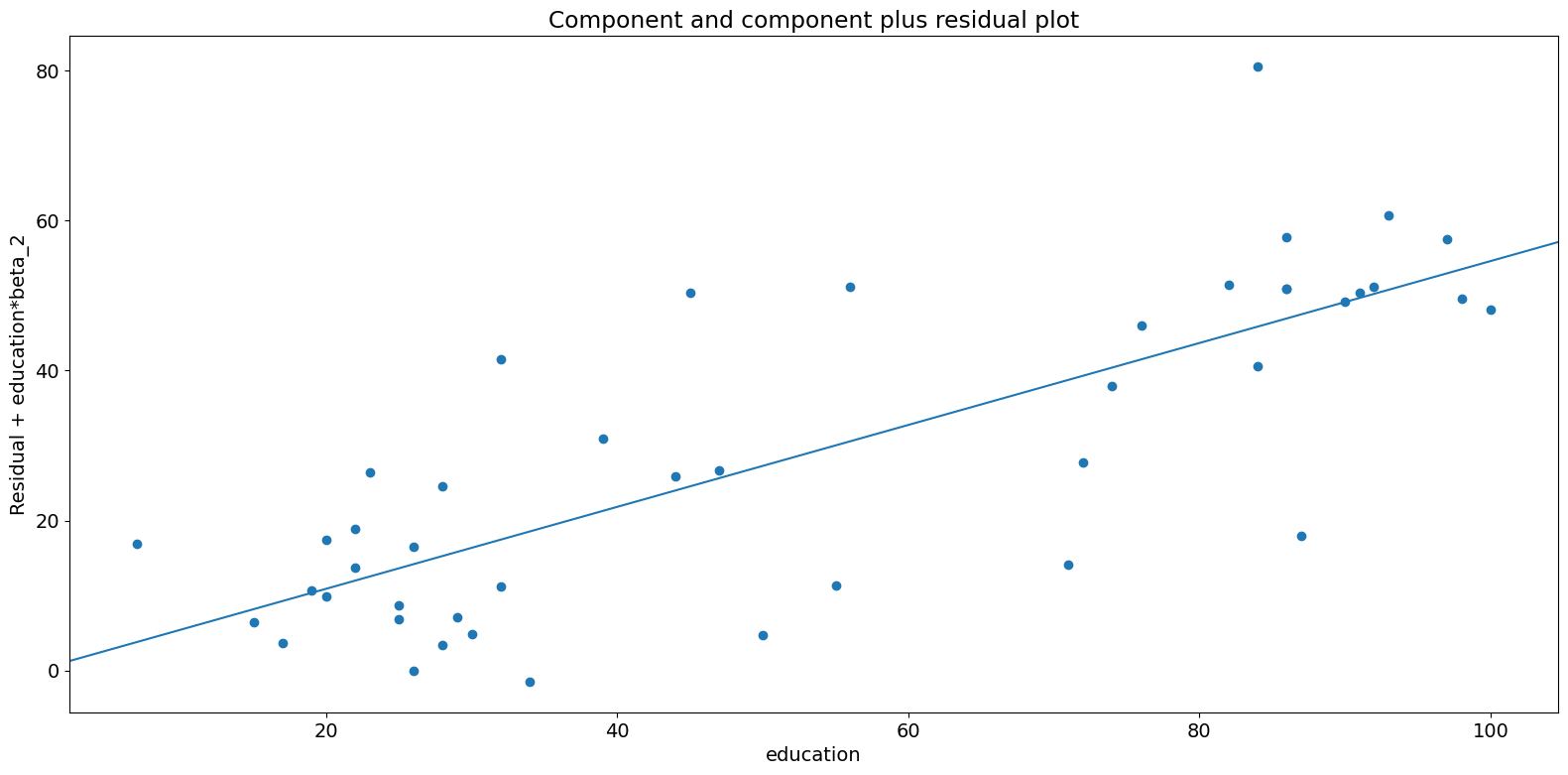

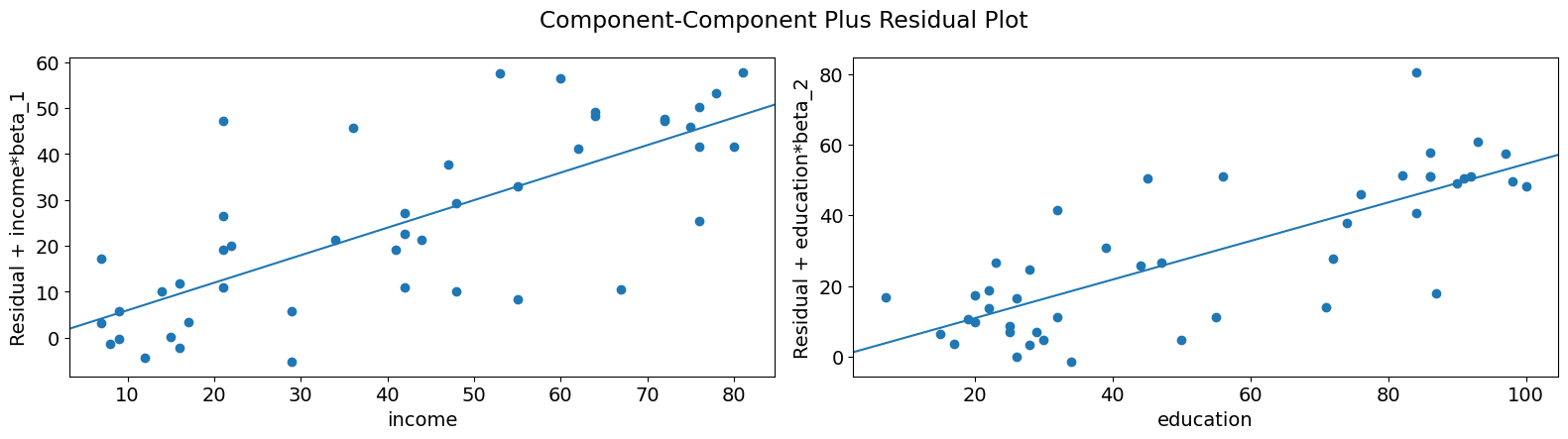

CCPR 图提供了一种方法来判断一个回归变量对响应变量的影响,方法是考虑其他自变量的影响。偏残差图定义为 \(\text{Residuals} + B_iX_i \text{ }\text{ }\) 对 \(X_i\) 的图。该成分添加了 \(B_iX_i\) 对 \(X_i\) 的图,以显示拟合线的位置。如果 \(X_i\) 与任何其他自变量高度相关,则应小心。如果是这种情况,图中明显的方差将是真实方差的低估。

[12]:

fig = sm.graphics.plot_ccpr(prestige_model, "education")

fig.tight_layout(pad=1.0)

正如你所看到的,受教育程度解释的声望变化与收入条件下的关系似乎是线性的,尽管你可以看到有一些观测值对关系产生了相当大的影响。我们可以使用 plot_ccpr_grid 快速查看多个变量。

[13]:

fig = sm.graphics.plot_ccpr_grid(prestige_model)

fig.tight_layout(pad=1.0)

单变量回归诊断¶

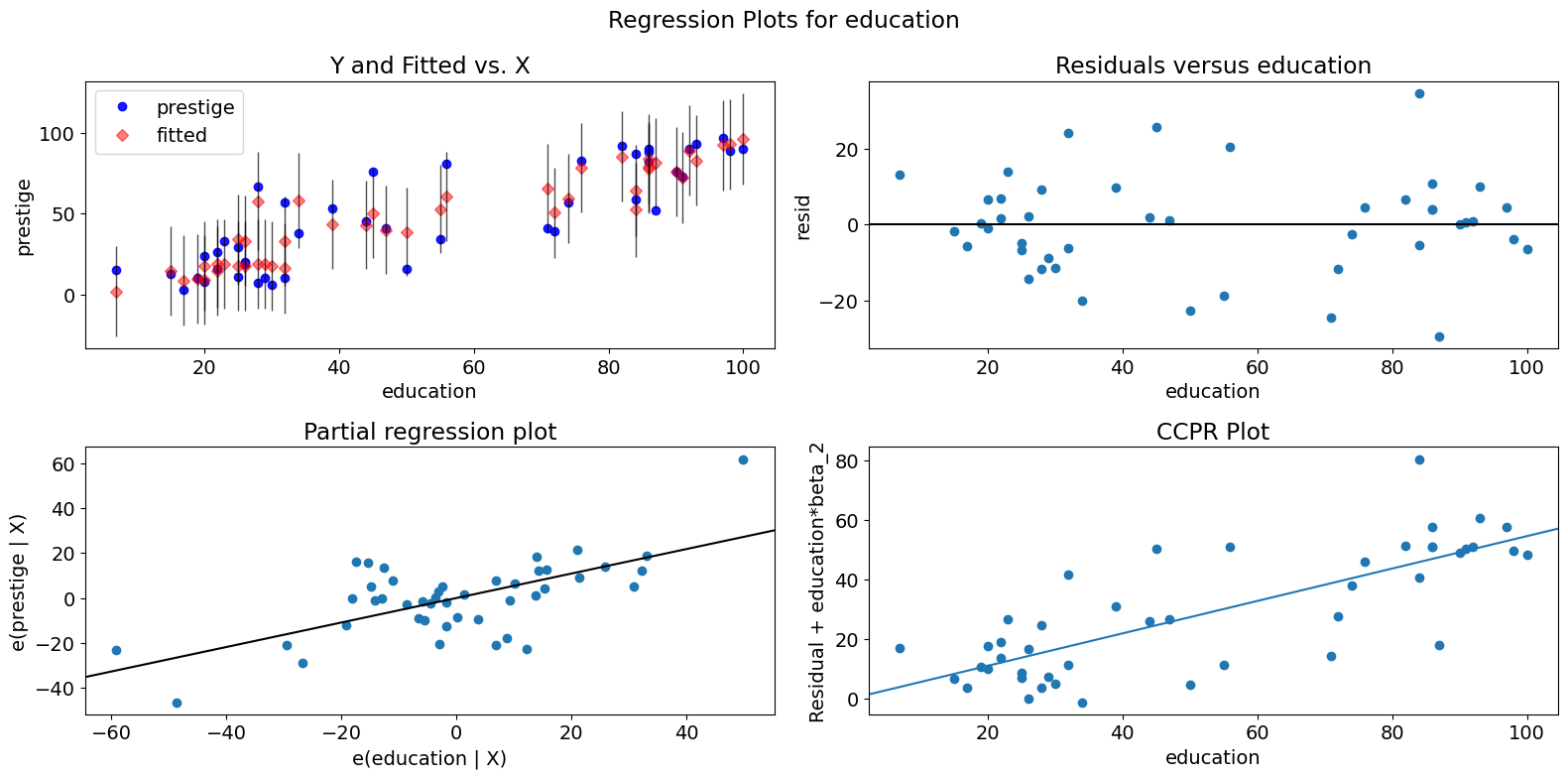

plot_regress_exog 函数是一个方便的函数,它提供了一个 2x2 图,包含因变量和拟合值(带有置信区间)与所选自变量的关系,模型残差与所选自变量的关系,偏回归图以及 CCPR 图。该函数可用于快速检查模型对单个回归变量的假设。

[14]:

fig = sm.graphics.plot_regress_exog(prestige_model, "education")

fig.tight_layout(pad=1.0)

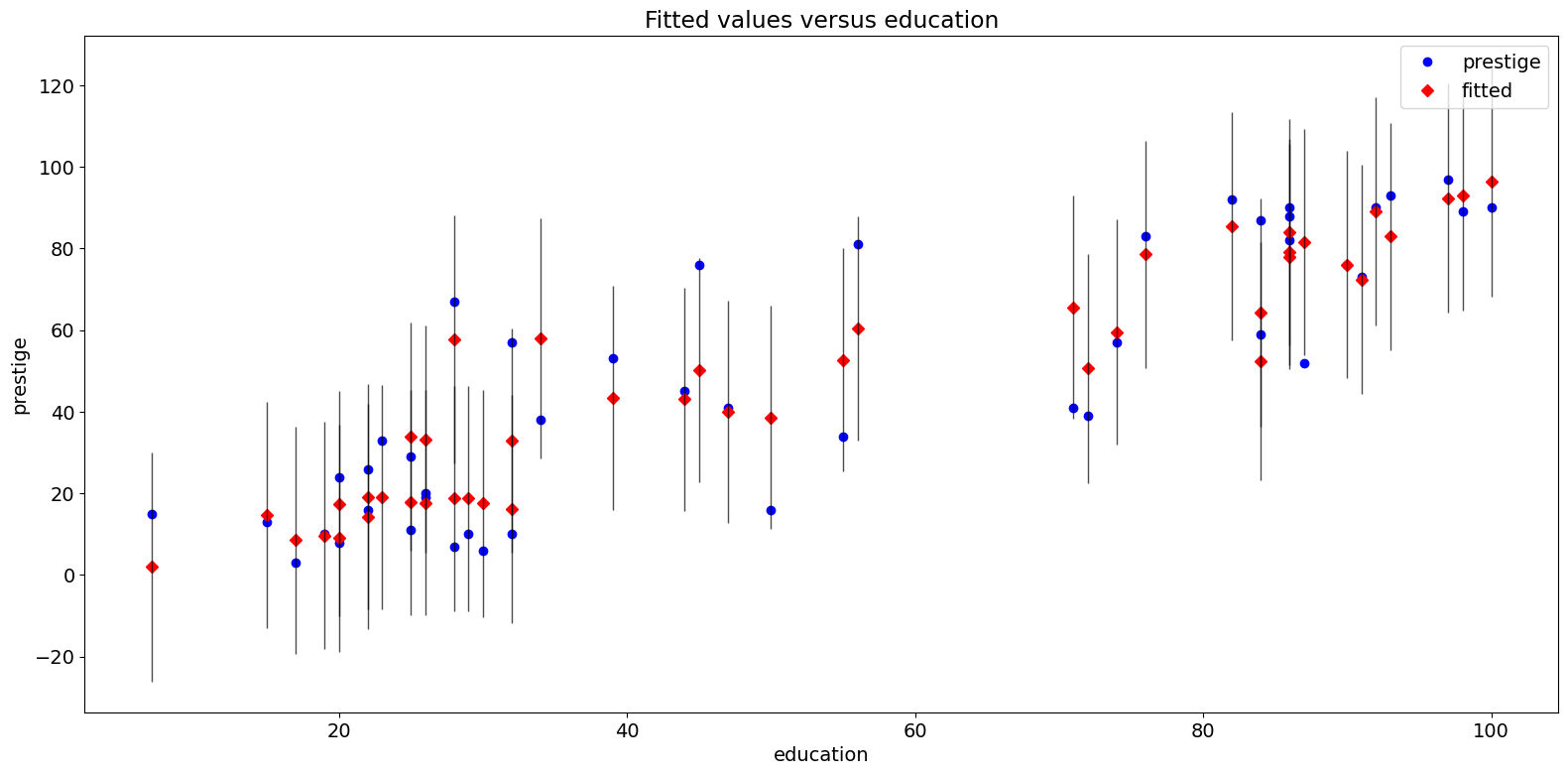

拟合图¶

plot_fit 函数绘制拟合值与所选自变量的关系。它包括预测置信区间,并且可以选择绘制真实的因变量。

[15]:

fig = sm.graphics.plot_fit(prestige_model, "education")

fig.tight_layout(pad=1.0)

2009 年全州犯罪数据集¶

将以下内容与 http://www.ats.ucla.edu/stat/stata/webbooks/reg/chapter4/statareg_self_assessment_answers4.htm 进行比较

虽然这里的数据与该示例中的数据不同。你可以通过取消注释下面必要的单元格来运行该示例。

[16]:

# dta = pd.read_csv("http://www.stat.ufl.edu/~aa/social/csv_files/statewide-crime-2.csv")

# dta = dta.set_index("State", inplace=True).dropna()

# dta.rename(columns={"VR" : "crime",

# "MR" : "murder",

# "M" : "pctmetro",

# "W" : "pctwhite",

# "H" : "pcths",

# "P" : "poverty",

# "S" : "single"

# }, inplace=True)

#

# crime_model = ols("murder ~ pctmetro + poverty + pcths + single", data=dta).fit()

[17]:

dta = sm.datasets.statecrime.load_pandas().data

[18]:

crime_model = ols("murder ~ urban + poverty + hs_grad + single", data=dta).fit()

print(crime_model.summary())

OLS Regression Results

==============================================================================

Dep. Variable: murder R-squared: 0.813

Model: OLS Adj. R-squared: 0.797

Method: Least Squares F-statistic: 50.08

Date: Thu, 03 Oct 2024 Prob (F-statistic): 3.42e-16

Time: 15:58:34 Log-Likelihood: -95.050

No. Observations: 51 AIC: 200.1

Df Residuals: 46 BIC: 209.8

Df Model: 4

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -44.1024 12.086 -3.649 0.001 -68.430 -19.774

urban 0.0109 0.015 0.707 0.483 -0.020 0.042

poverty 0.4121 0.140 2.939 0.005 0.130 0.694

hs_grad 0.3059 0.117 2.611 0.012 0.070 0.542

single 0.6374 0.070 9.065 0.000 0.496 0.779

==============================================================================

Omnibus: 1.618 Durbin-Watson: 2.507

Prob(Omnibus): 0.445 Jarque-Bera (JB): 0.831

Skew: -0.220 Prob(JB): 0.660

Kurtosis: 3.445 Cond. No. 5.80e+03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 5.8e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

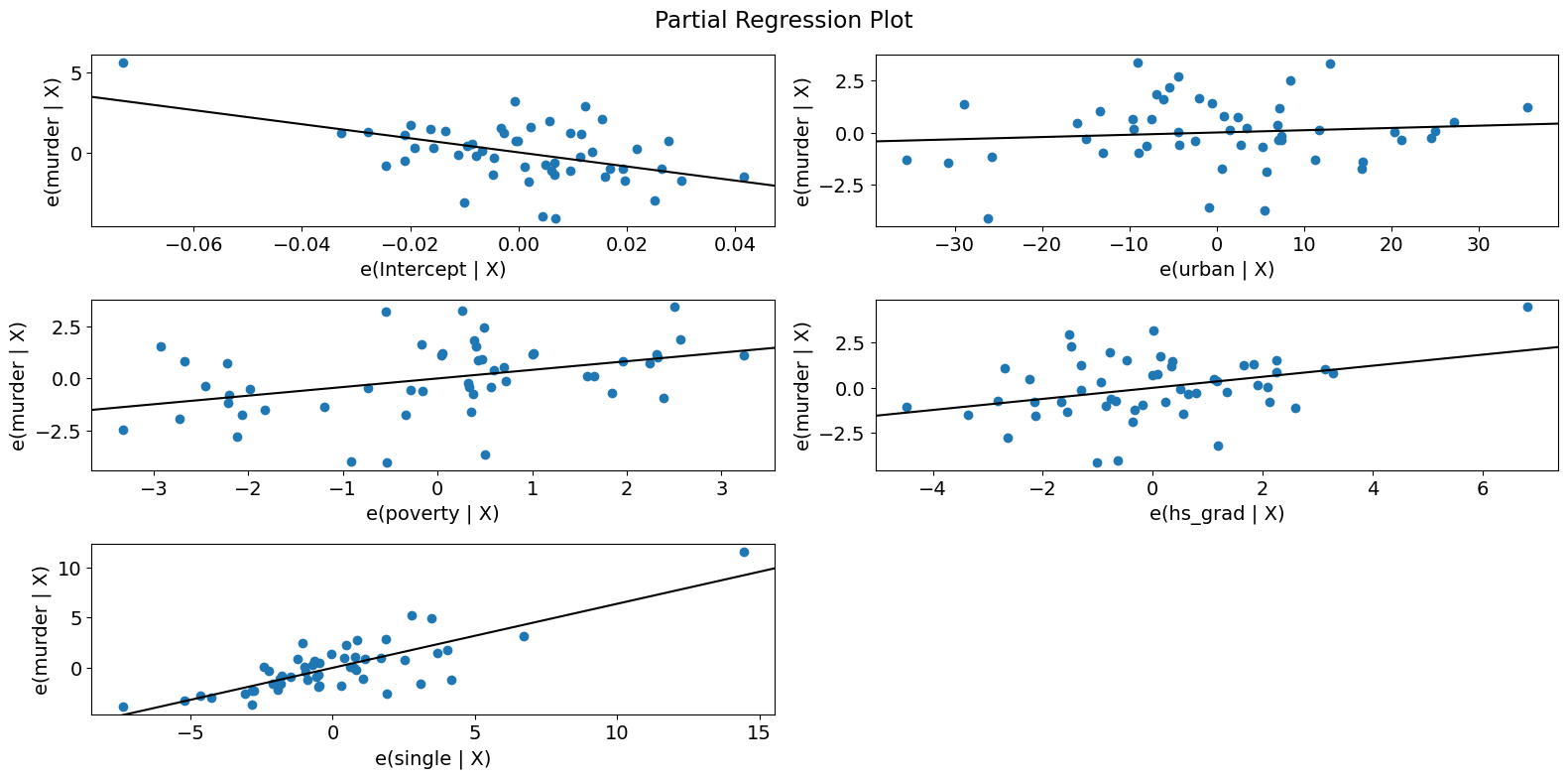

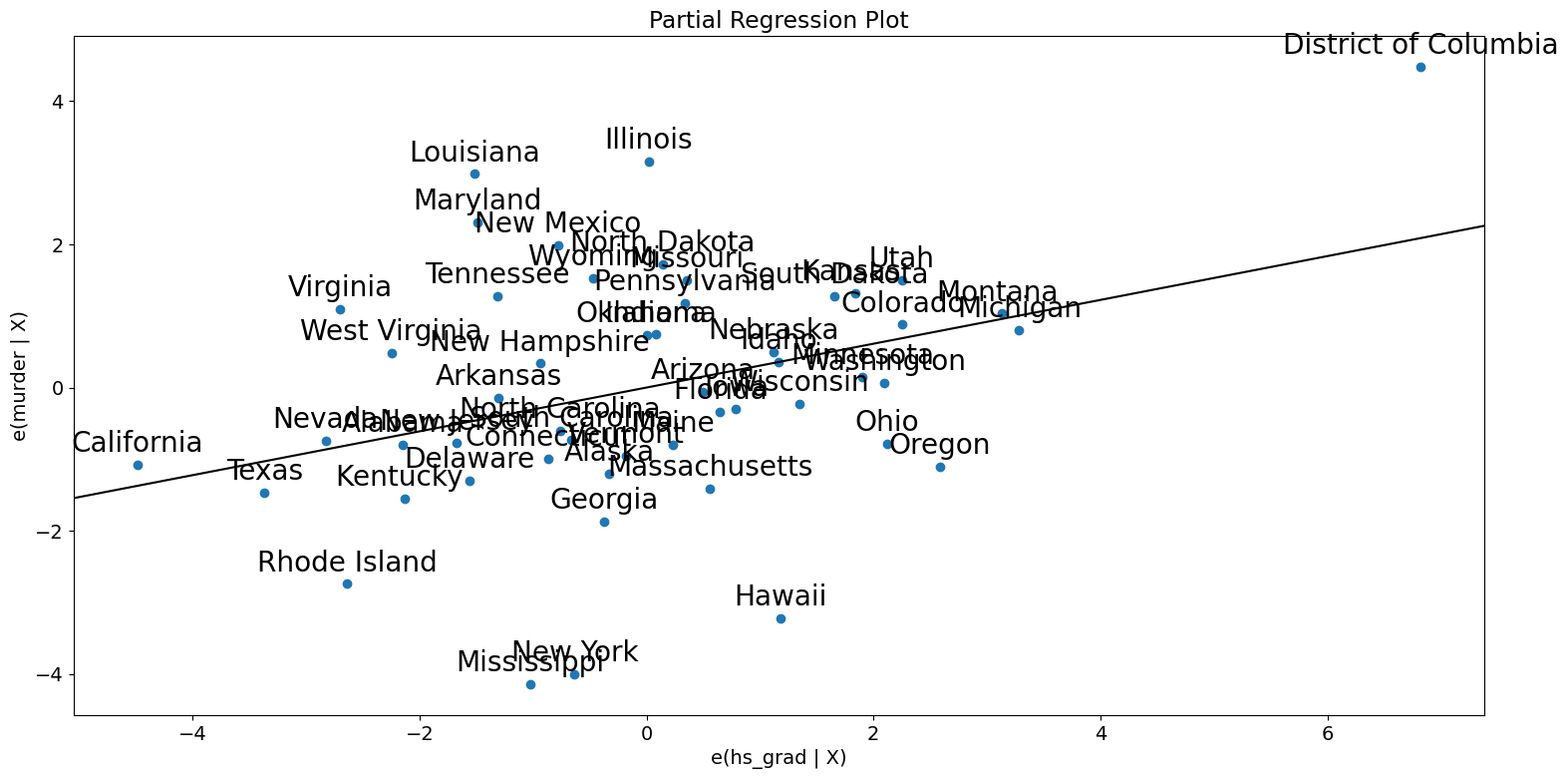

偏回归图 (犯罪数据)¶

[19]:

fig = sm.graphics.plot_partregress_grid(crime_model)

fig.tight_layout(pad=1.0)

[20]:

fig = sm.graphics.plot_partregress(

"murder", "hs_grad", ["urban", "poverty", "single"], data=dta

)

fig.tight_layout(pad=1.0)

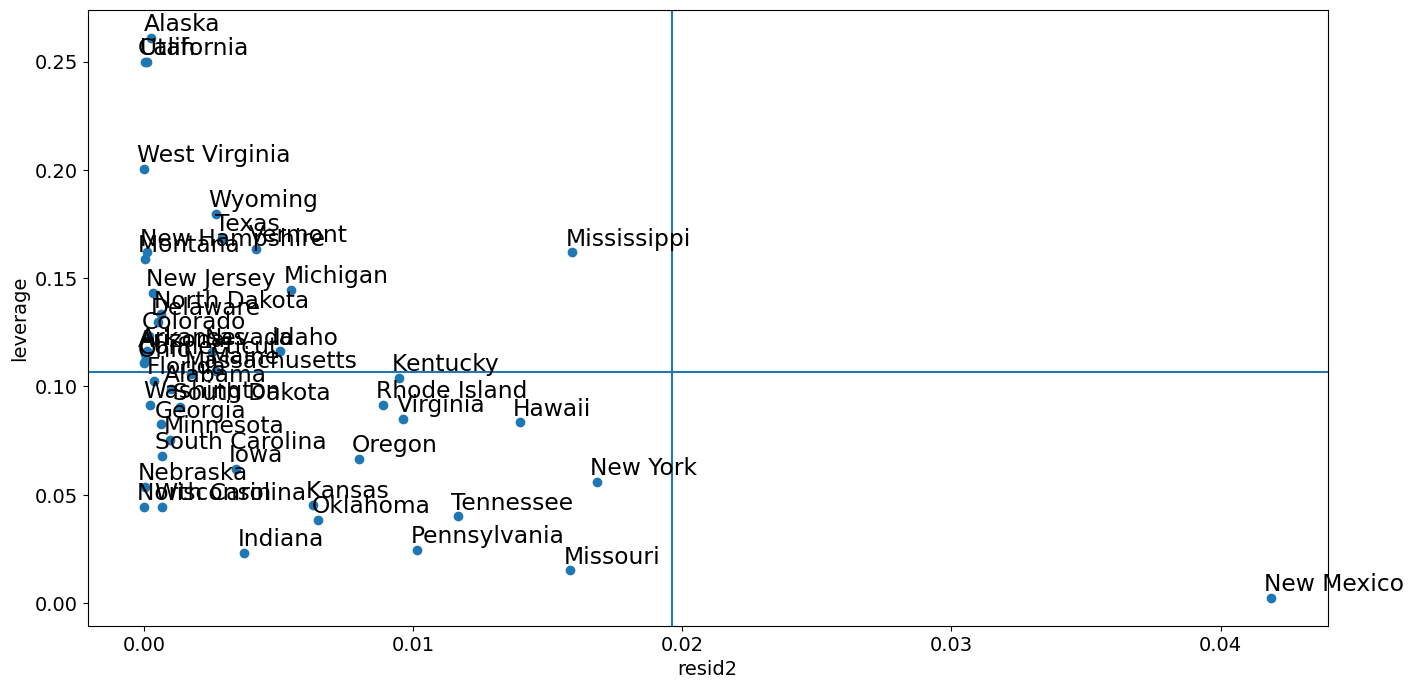

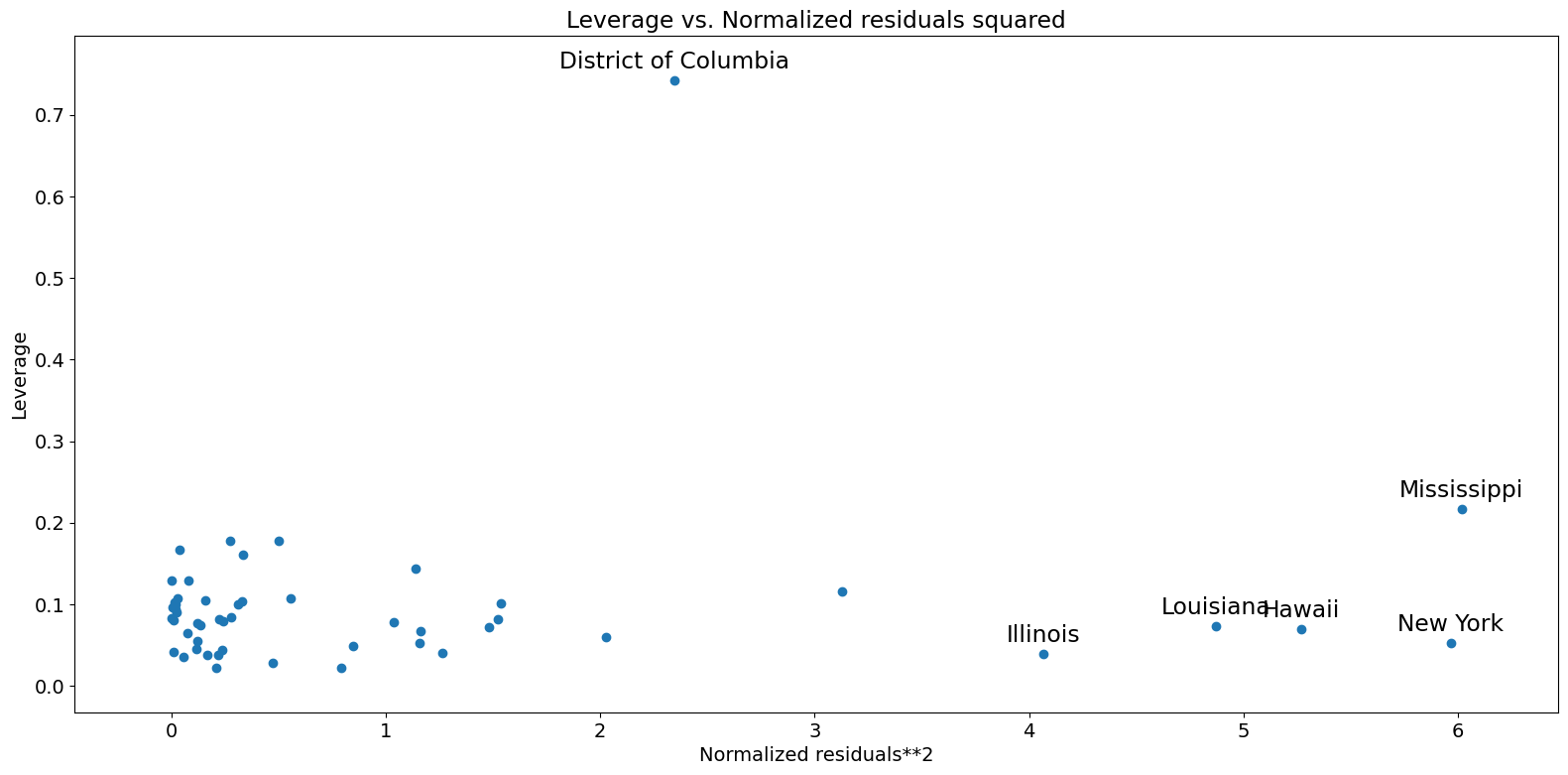

杠杆-残差平方图¶

与影响图密切相关的是杠杆-残差平方图。

[21]:

fig = sm.graphics.plot_leverage_resid2(crime_model)

fig.tight_layout(pad=1.0)

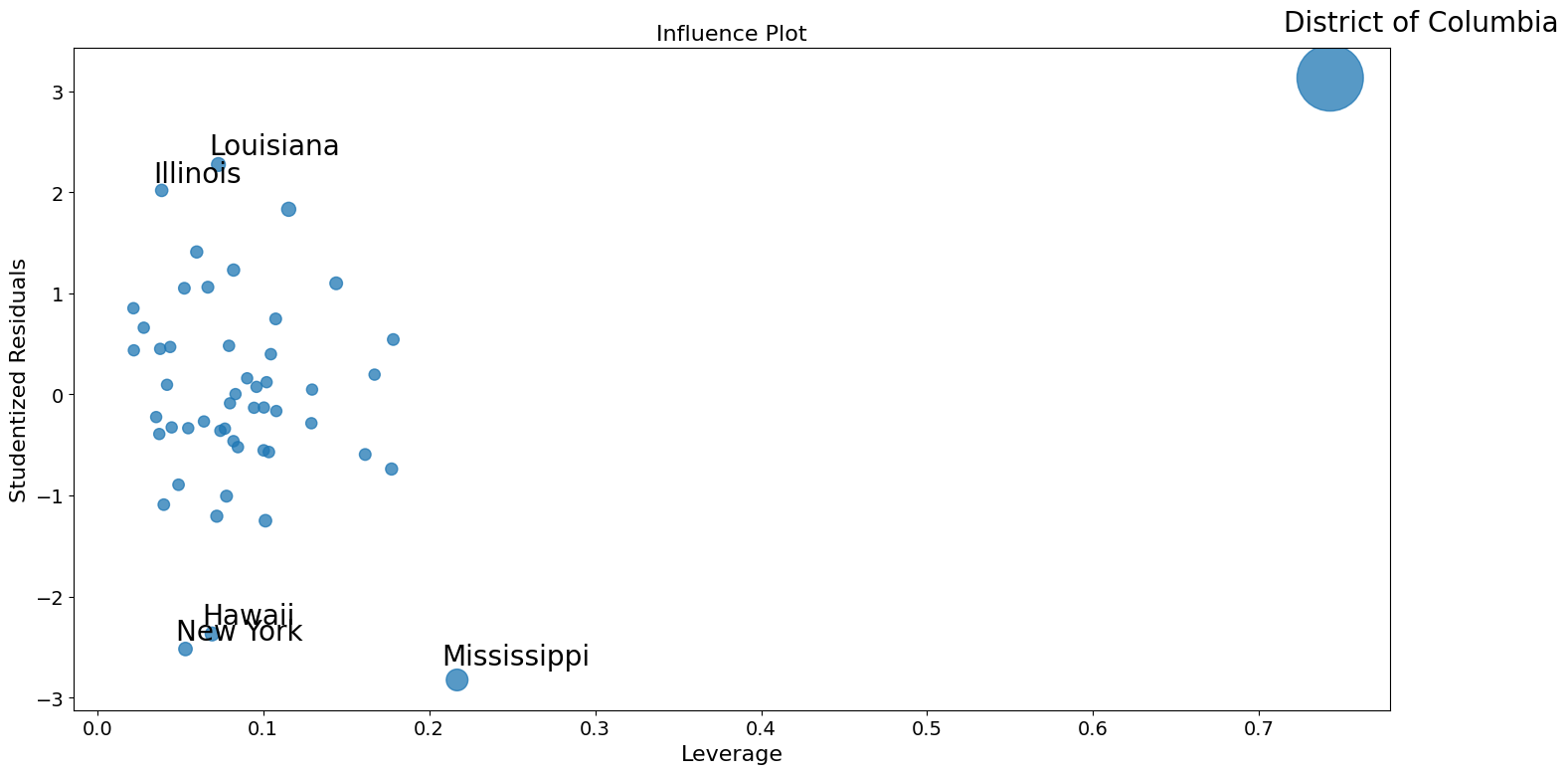

影响图¶

[22]:

fig = sm.graphics.influence_plot(crime_model)

fig.tight_layout(pad=1.0)

使用稳健回归来校正异常值。¶

这里重现 Stata 结果的一部分问题是,M 估计量对杠杆点不稳健。MM 估计量应该对这些示例更有效。

[23]:

from statsmodels.formula.api import rlm

[24]:

rob_crime_model = rlm(

"murder ~ urban + poverty + hs_grad + single",

data=dta,

M=sm.robust.norms.TukeyBiweight(3),

).fit(conv="weights")

print(rob_crime_model.summary())

Robust linear Model Regression Results

==============================================================================

Dep. Variable: murder No. Observations: 51

Model: RLM Df Residuals: 46

Method: IRLS Df Model: 4

Norm: TukeyBiweight

Scale Est.: mad

Cov Type: H1

Date: Thu, 03 Oct 2024

Time: 15:58:38

No. Iterations: 50

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -4.2986 9.494 -0.453 0.651 -22.907 14.310

urban 0.0029 0.012 0.241 0.809 -0.021 0.027

poverty 0.2753 0.110 2.499 0.012 0.059 0.491

hs_grad -0.0302 0.092 -0.328 0.743 -0.211 0.150

single 0.2902 0.055 5.253 0.000 0.182 0.398

==============================================================================

If the model instance has been used for another fit with different fit parameters, then the fit options might not be the correct ones anymore .

[25]:

# rob_crime_model = rlm("murder ~ pctmetro + poverty + pcths + single", data=dta, M=sm.robust.norms.TukeyBiweight()).fit(conv="weights")

# print(rob_crime_model.summary())

RLM 中还没有影响诊断方法,但我们可以重新创建它们。(这取决于 issue #888 的状态)

[26]:

weights = rob_crime_model.weights

idx = weights > 0

X = rob_crime_model.model.exog[idx.values]

ww = weights[idx] / weights[idx].mean()

hat_matrix_diag = ww * (X * np.linalg.pinv(X).T).sum(1)

resid = rob_crime_model.resid

resid2 = resid ** 2

resid2 /= resid2.sum()

nobs = int(idx.sum())

hm = hat_matrix_diag.mean()

rm = resid2.mean()

[27]:

from statsmodels.graphics import utils

fig, ax = plt.subplots(figsize=(16, 8))

ax.plot(resid2[idx], hat_matrix_diag, "o")

ax = utils.annotate_axes(

range(nobs),

labels=rob_crime_model.model.data.row_labels[idx],

points=lzip(resid2[idx], hat_matrix_diag),

offset_points=[(-5, 5)] * nobs,

size="large",

ax=ax,

)

ax.set_xlabel("resid2")

ax.set_ylabel("leverage")

ylim = ax.get_ylim()

ax.vlines(rm, *ylim)

xlim = ax.get_xlim()

ax.hlines(hm, *xlim)

ax.margins(0, 0)