使用 LOESS 进行季节性趋势分解 (STL)¶

此笔记本演示了 STL 的使用,它将时间序列分解为三个部分:趋势、季节性和残差。STL 使用 LOESS(局部加权回归)来提取三个部分的平滑估计。 STL 的关键输入是

season- 季节性平滑器的长度。必须为奇数。trend- 趋势平滑器的长度,通常约为season的 150%。必须为奇数且大于season。low_pass- 低通估计窗口的长度,通常是大于数据周期性的最小奇数。

首先,我们导入所需的包,准备图形环境并准备数据。

[1]:

import matplotlib.pyplot as plt

import pandas as pd

import seaborn as sns

from pandas.plotting import register_matplotlib_converters

register_matplotlib_converters()

sns.set_style("darkgrid")

[2]:

plt.rc("figure", figsize=(16, 12))

plt.rc("font", size=13)

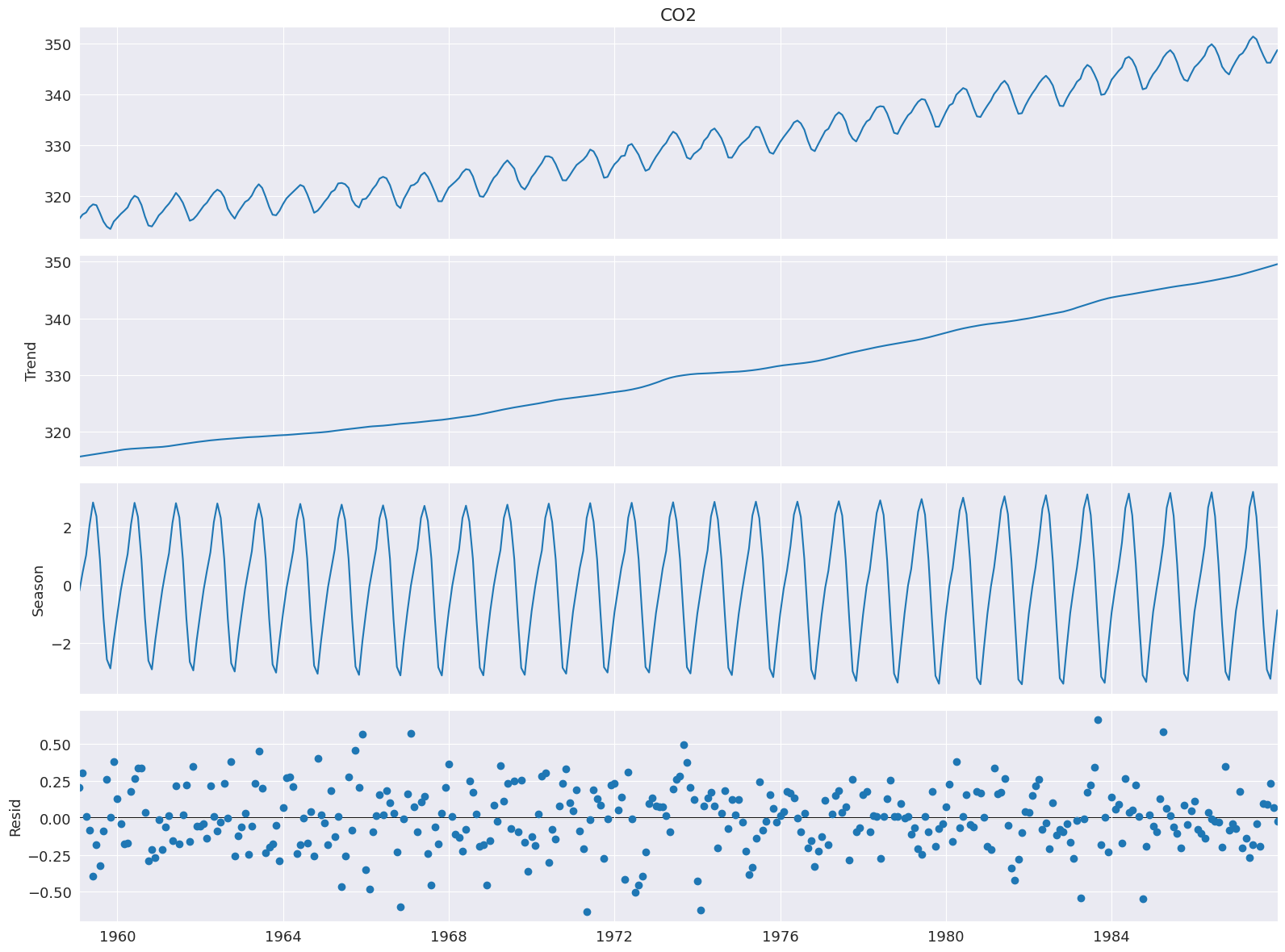

大气 CO2¶

Cleveland、Cleveland、McRae 和 Terpenning(1990 年)的示例使用 CO2 数据,这些数据在下面的列表中。此月度数据(1959 年 1 月至 1987 年 12 月)在整个样本中具有明显的趋势和季节性。

[3]:

co2 = [

315.58,

316.39,

316.79,

317.82,

318.39,

318.22,

316.68,

315.01,

314.02,

313.55,

315.02,

315.75,

316.52,

317.10,

317.79,

319.22,

320.08,

319.70,

318.27,

315.99,

314.24,

314.05,

315.05,

316.23,

316.92,

317.76,

318.54,

319.49,

320.64,

319.85,

318.70,

316.96,

315.17,

315.47,

316.19,

317.17,

318.12,

318.72,

319.79,

320.68,

321.28,

320.89,

319.79,

317.56,

316.46,

315.59,

316.85,

317.87,

318.87,

319.25,

320.13,

321.49,

322.34,

321.62,

319.85,

317.87,

316.36,

316.24,

317.13,

318.46,

319.57,

320.23,

320.89,

321.54,

322.20,

321.90,

320.42,

318.60,

316.73,

317.15,

317.94,

318.91,

319.73,

320.78,

321.23,

322.49,

322.59,

322.35,

321.61,

319.24,

318.23,

317.76,

319.36,

319.50,

320.35,

321.40,

322.22,

323.45,

323.80,

323.50,

322.16,

320.09,

318.26,

317.66,

319.47,

320.70,

322.06,

322.23,

322.78,

324.10,

324.63,

323.79,

322.34,

320.73,

319.00,

318.99,

320.41,

321.68,

322.30,

322.89,

323.59,

324.65,

325.30,

325.15,

323.88,

321.80,

319.99,

319.86,

320.88,

322.36,

323.59,

324.23,

325.34,

326.33,

327.03,

326.24,

325.39,

323.16,

321.87,

321.31,

322.34,

323.74,

324.61,

325.58,

326.55,

327.81,

327.82,

327.53,

326.29,

324.66,

323.12,

323.09,

324.01,

325.10,

326.12,

326.62,

327.16,

327.94,

329.15,

328.79,

327.53,

325.65,

323.60,

323.78,

325.13,

326.26,

326.93,

327.84,

327.96,

329.93,

330.25,

329.24,

328.13,

326.42,

324.97,

325.29,

326.56,

327.73,

328.73,

329.70,

330.46,

331.70,

332.66,

332.22,

331.02,

329.39,

327.58,

327.27,

328.30,

328.81,

329.44,

330.89,

331.62,

332.85,

333.29,

332.44,

331.35,

329.58,

327.58,

327.55,

328.56,

329.73,

330.45,

330.98,

331.63,

332.88,

333.63,

333.53,

331.90,

330.08,

328.59,

328.31,

329.44,

330.64,

331.62,

332.45,

333.36,

334.46,

334.84,

334.29,

333.04,

330.88,

329.23,

328.83,

330.18,

331.50,

332.80,

333.22,

334.54,

335.82,

336.45,

335.97,

334.65,

332.40,

331.28,

330.73,

332.05,

333.54,

334.65,

335.06,

336.32,

337.39,

337.66,

337.56,

336.24,

334.39,

332.43,

332.22,

333.61,

334.78,

335.88,

336.43,

337.61,

338.53,

339.06,

338.92,

337.39,

335.72,

333.64,

333.65,

335.07,

336.53,

337.82,

338.19,

339.89,

340.56,

341.22,

340.92,

339.26,

337.27,

335.66,

335.54,

336.71,

337.79,

338.79,

340.06,

340.93,

342.02,

342.65,

341.80,

340.01,

337.94,

336.17,

336.28,

337.76,

339.05,

340.18,

341.04,

342.16,

343.01,

343.64,

342.91,

341.72,

339.52,

337.75,

337.68,

339.14,

340.37,

341.32,

342.45,

343.05,

344.91,

345.77,

345.30,

343.98,

342.41,

339.89,

340.03,

341.19,

342.87,

343.74,

344.55,

345.28,

347.00,

347.37,

346.74,

345.36,

343.19,

340.97,

341.20,

342.76,

343.96,

344.82,

345.82,

347.24,

348.09,

348.66,

347.90,

346.27,

344.21,

342.88,

342.58,

343.99,

345.31,

345.98,

346.72,

347.63,

349.24,

349.83,

349.10,

347.52,

345.43,

344.48,

343.89,

345.29,

346.54,

347.66,

348.07,

349.12,

350.55,

351.34,

350.80,

349.10,

347.54,

346.20,

346.20,

347.44,

348.67,

]

co2 = pd.Series(

co2, index=pd.date_range("1-1-1959", periods=len(co2), freq="M"), name="CO2"

)

co2.describe()

/tmp/ipykernel_3881/1071343913.py:352: FutureWarning: 'M' is deprecated and will be removed in a future version, please use 'ME' instead.

co2, index=pd.date_range("1-1-1959", periods=len(co2), freq="M"), name="CO2"

[3]:

count 348.000000

mean 330.123879

std 10.059747

min 313.550000

25% 321.302500

50% 328.820000

75% 338.002500

max 351.340000

Name: CO2, dtype: float64

分解需要 1 个输入,即数据序列。如果数据序列没有频率,那么你还必须指定 period。 seasonal 的默认值为 7,因此在大多数应用程序中也应该更改。

[4]:

from statsmodels.tsa.seasonal import STL

stl = STL(co2, seasonal=13)

res = stl.fit()

fig = res.plot()

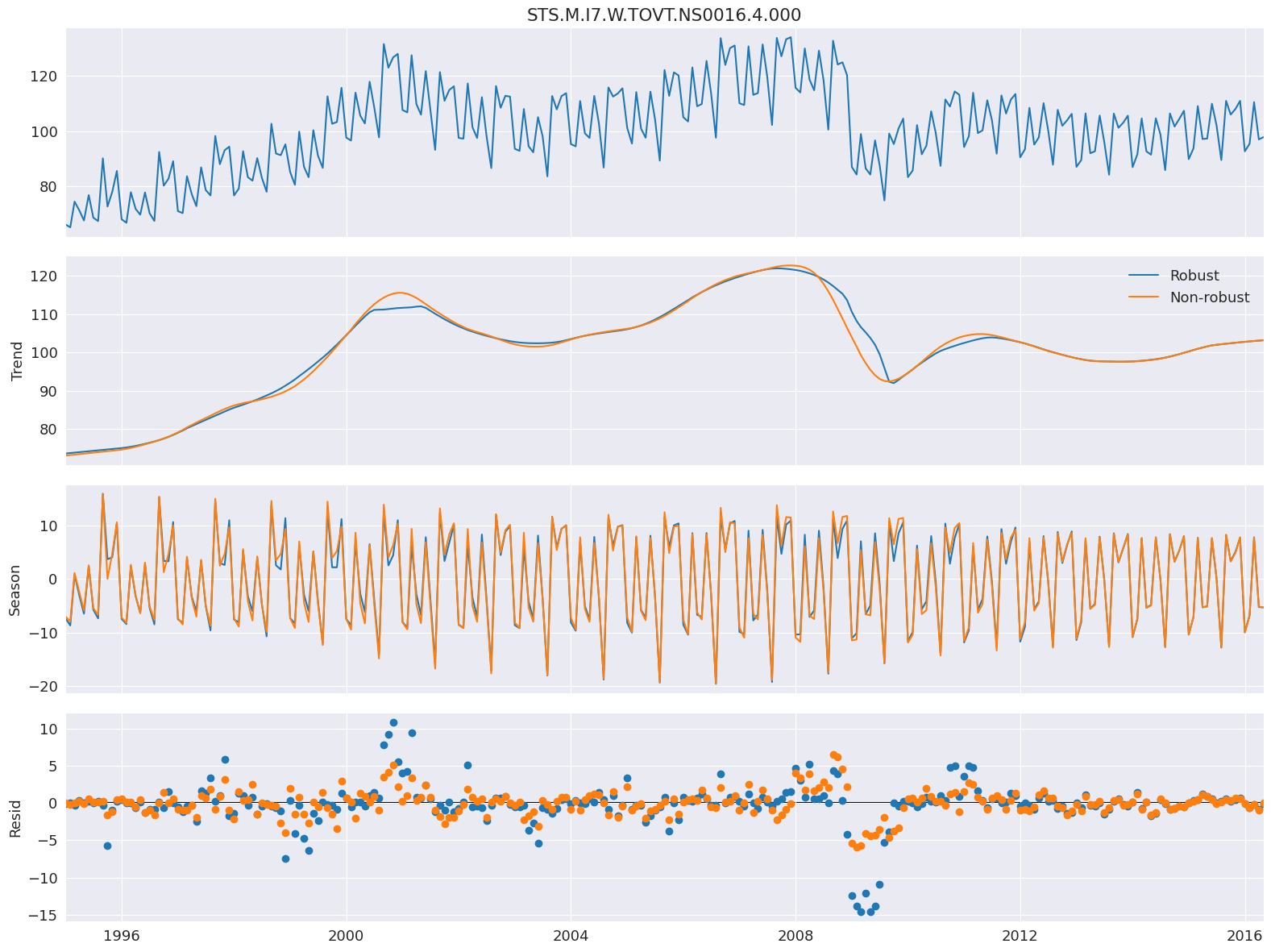

稳健拟合¶

设置 robust 将使用数据依赖的加权函数,该函数在估计 LOESS 时重新加权数据(因此使用 LOWESS)。使用稳健估计允许模型容忍在底部图中可见的较大误差。

这里我们使用一个测量欧盟电气设备生产量的序列。

[5]:

from statsmodels.datasets import elec_equip as ds

elec_equip = ds.load().data.iloc[:, 0]

接下来,我们使用和不使用稳健加权估计模型。差异很小,在 2008 年金融危机期间最为明显。非稳健估计对所有观察结果赋予相同的权重,因此平均产生较小的误差。权重在 0 到 1 之间变化。

[6]:

def add_stl_plot(fig, res, legend):

"""Add 3 plots from a second STL fit"""

axs = fig.get_axes()

comps = ["trend", "seasonal", "resid"]

for ax, comp in zip(axs[1:], comps):

series = getattr(res, comp)

if comp == "resid":

ax.plot(series, marker="o", linestyle="none")

else:

ax.plot(series)

if comp == "trend":

ax.legend(legend, frameon=False)

stl = STL(elec_equip, period=12, robust=True)

res_robust = stl.fit()

fig = res_robust.plot()

res_non_robust = STL(elec_equip, period=12, robust=False).fit()

add_stl_plot(fig, res_non_robust, ["Robust", "Non-robust"])

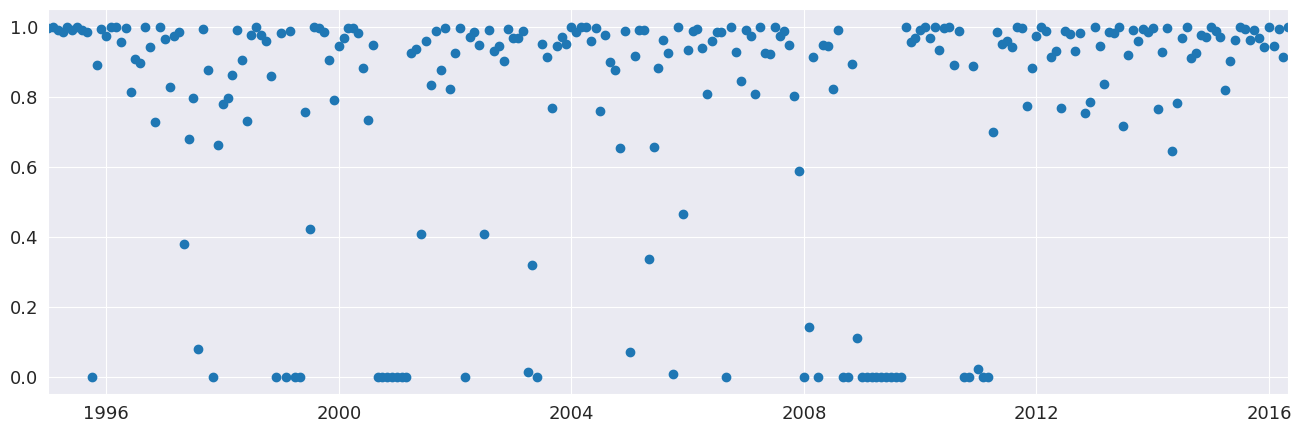

[7]:

fig = plt.figure(figsize=(16, 5))

lines = plt.plot(res_robust.weights, marker="o", linestyle="none")

ax = plt.gca()

xlim = ax.set_xlim(elec_equip.index[0], elec_equip.index[-1])

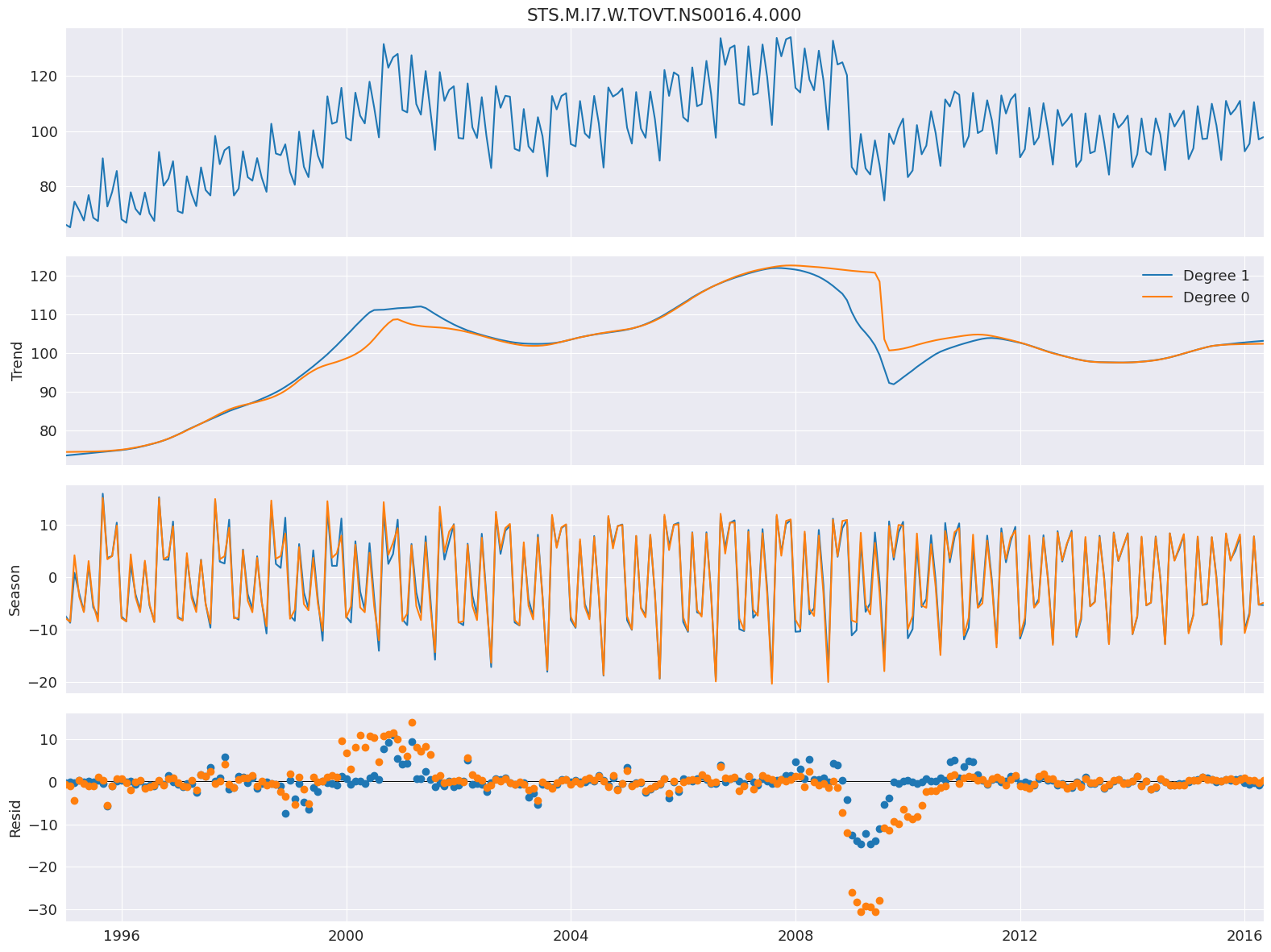

LOESS 度数¶

默认配置使用常数和趋势来估计 LOESS 模型。可以通过将 COMPONENT_deg 设置为 0 来更改为仅包含常数。这里,度数几乎没有区别,除了在 2008 年金融危机期间的趋势之外。

[8]:

stl = STL(

elec_equip, period=12, seasonal_deg=0, trend_deg=0, low_pass_deg=0, robust=True

)

res_deg_0 = stl.fit()

fig = res_robust.plot()

add_stl_plot(fig, res_deg_0, ["Degree 1", "Degree 0"])

性能¶

可以使用三种选项来降低 STL 分解的计算成本

seasonal_jumptrend_jumplow_pass_jump

当这些值不为零时,组件 COMPONENT 的 LOESS 仅在每 COMPONENT_jump 个观察值进行估计,并且在点之间使用线性插值。这些值通常不应超过 seasonal、trend 或 low_pass 大小的 10-20%。

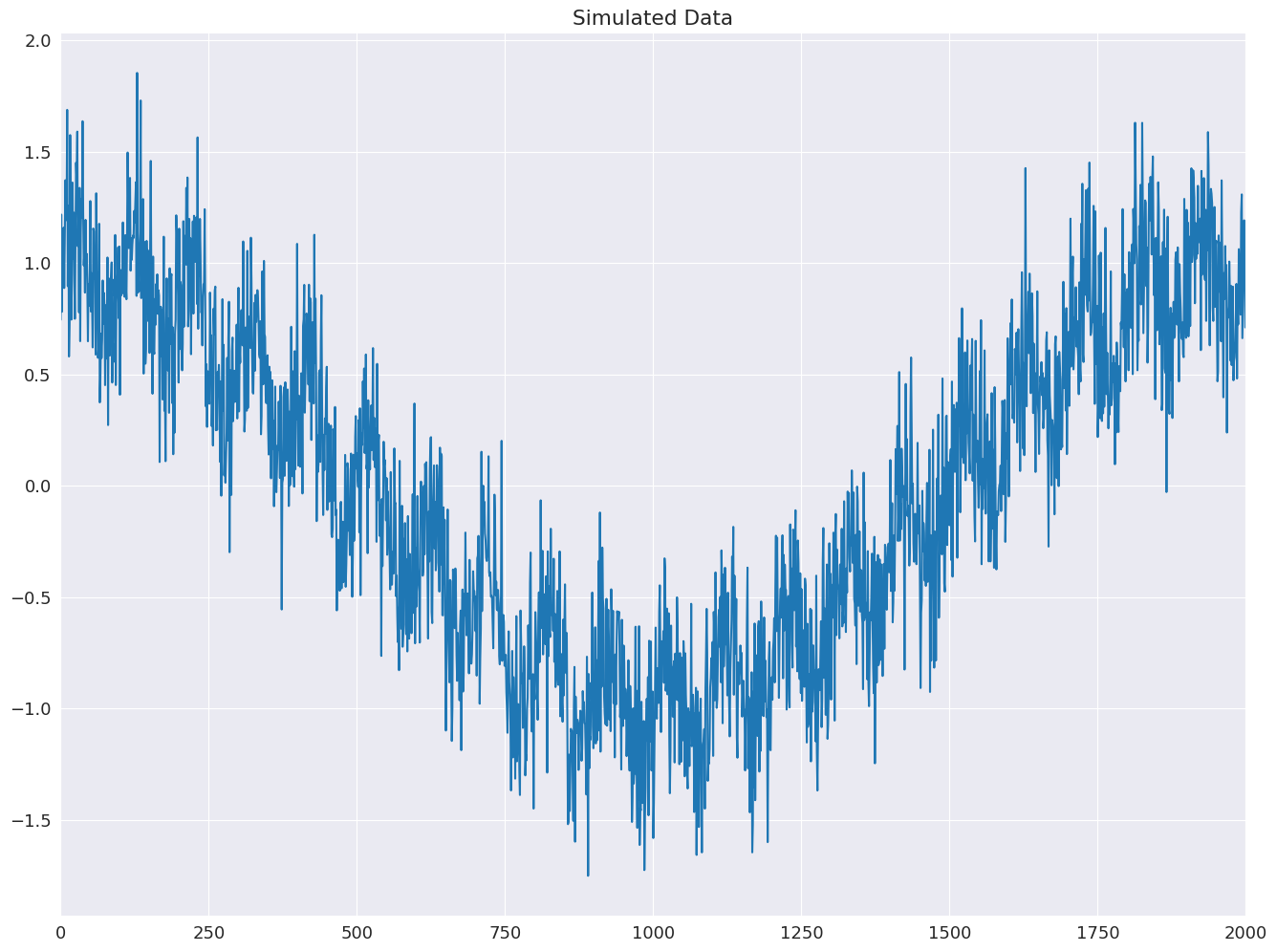

下面的示例展示了如何使用模拟数据(具有低频余弦趋势和正弦季节模式)将计算成本降低 15 倍。

[9]:

import numpy as np

rs = np.random.RandomState(0xA4FD94BC)

tau = 2000

t = np.arange(tau)

period = int(0.05 * tau)

seasonal = period + ((period % 2) == 0) # Ensure odd

e = 0.25 * rs.standard_normal(tau)

y = np.cos(t / tau * 2 * np.pi) + 0.25 * np.sin(t / period * 2 * np.pi) + e

plt.plot(y)

plt.title("Simulated Data")

xlim = plt.gca().set_xlim(0, tau)

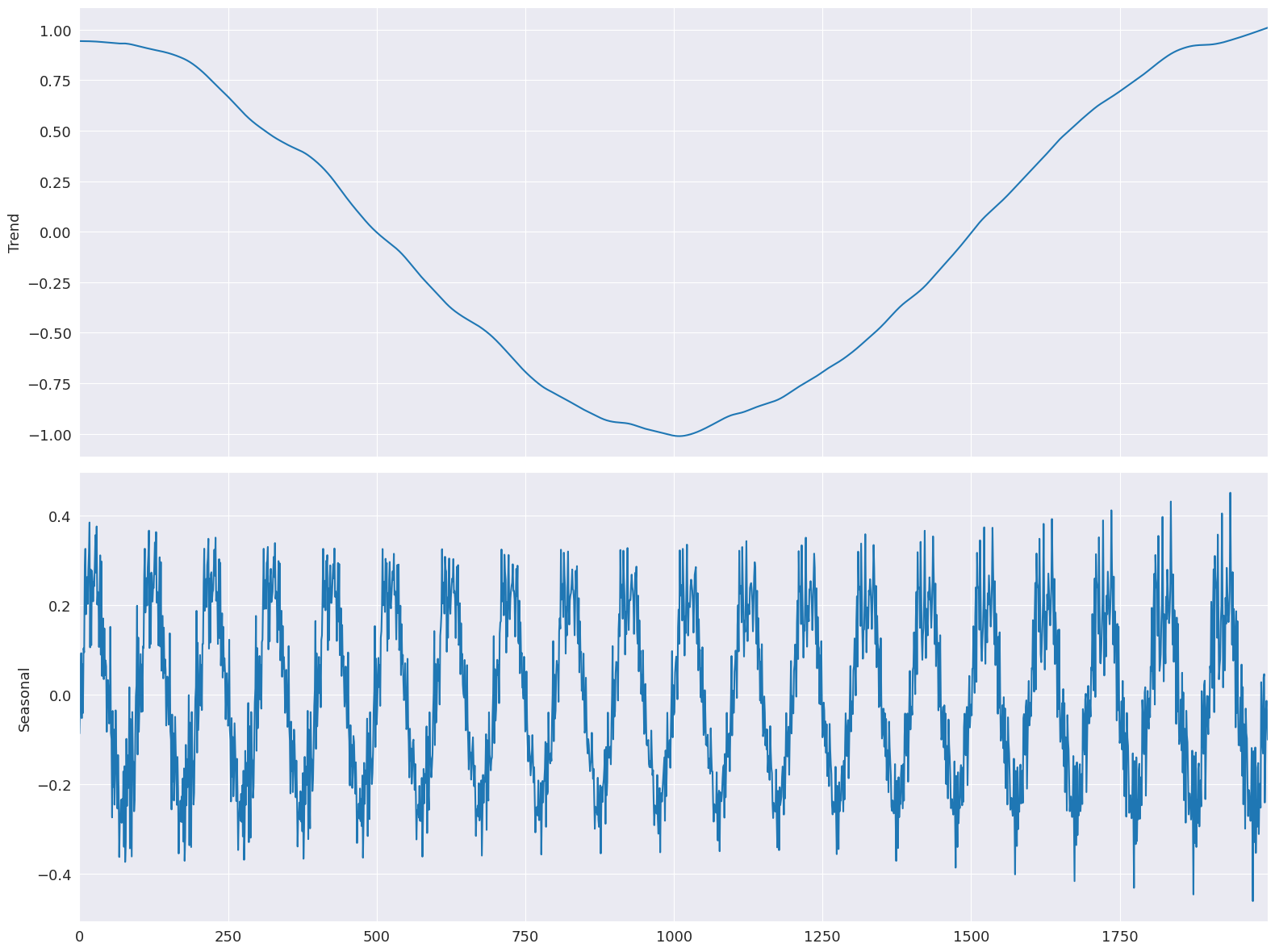

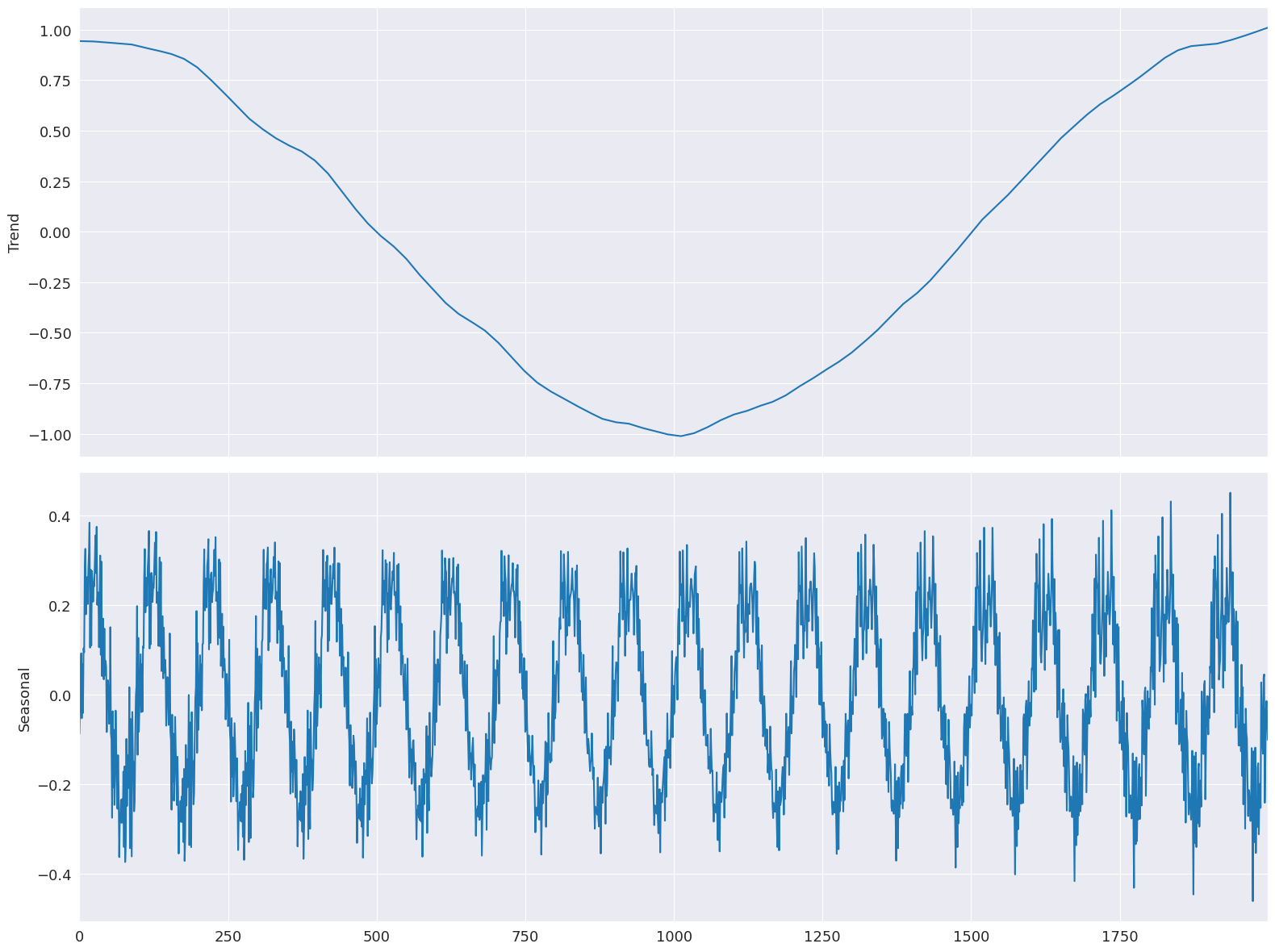

首先,使用所有跳跃都等于 1 来估计基线模型。

[10]:

mod = STL(y, period=period, seasonal=seasonal)

%timeit mod.fit()

res = mod.fit()

fig = res.plot(observed=False, resid=False)

284 ms ± 38.9 ms per loop (mean ± std. dev. of 7 runs, 1 loop each)

所有跳跃都设置为其窗口长度的 15%。有限的线性插值对模型的拟合几乎没有影响。

[11]:

low_pass_jump = seasonal_jump = int(0.15 * (period + 1))

trend_jump = int(0.15 * 1.5 * (period + 1))

mod = STL(

y,

period=period,

seasonal=seasonal,

seasonal_jump=seasonal_jump,

trend_jump=trend_jump,

low_pass_jump=low_pass_jump,

)

%timeit mod.fit()

res = mod.fit()

fig = res.plot(observed=False, resid=False)

22.9 ms ± 1.04 ms per loop (mean ± std. dev. of 7 runs, 10 loops each)

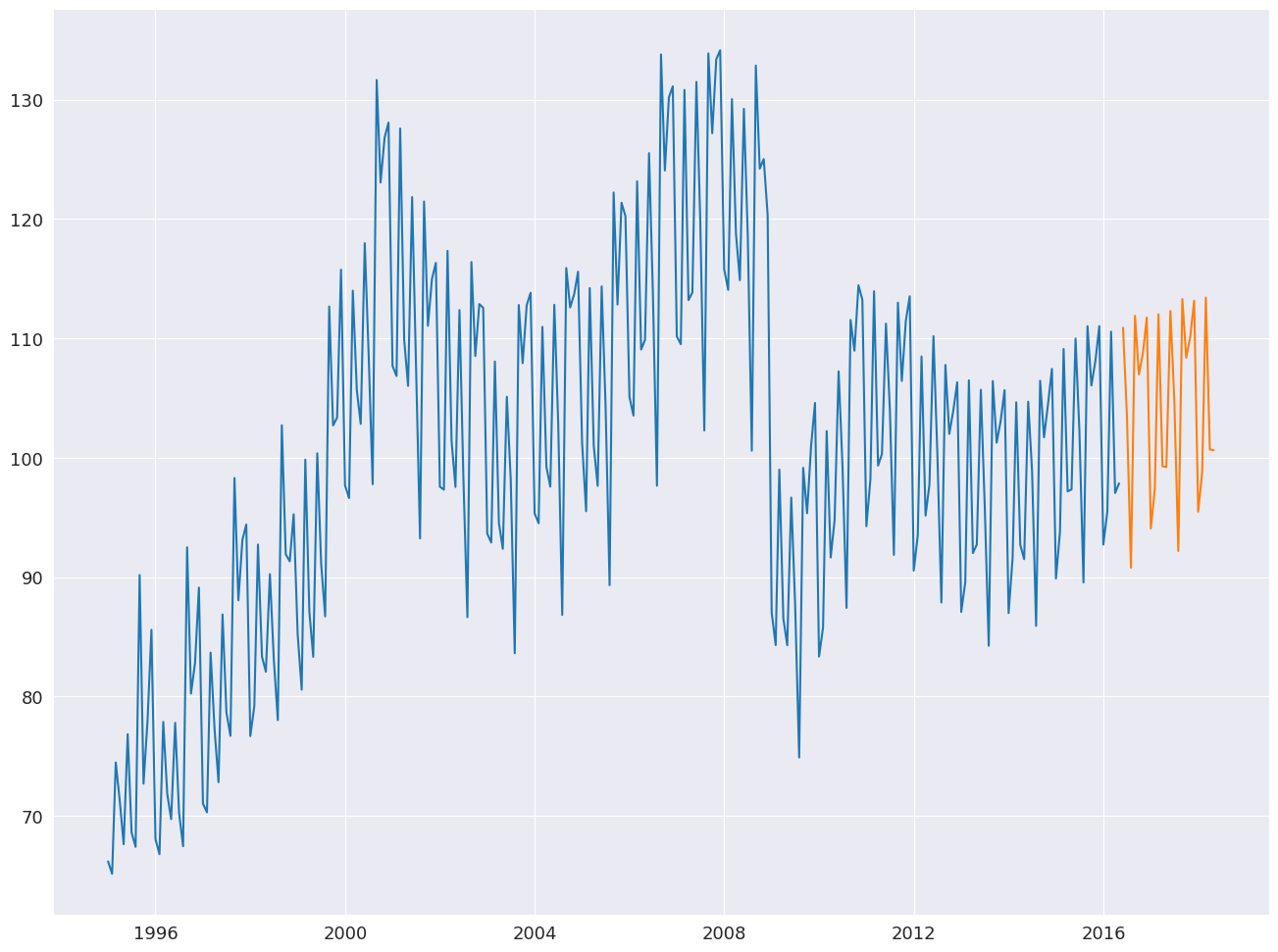

使用 STL 进行预测¶

STLForecast 简化了使用 STL 来消除季节性,然后使用标准时间序列模型来预测趋势和循环部分的过程。

这里,我们使用 STL 来处理季节性,然后使用 ARIMA(1,1,0) 来建模去季节化数据。季节性成分是根据找到的完整周期进行预测的,其中

其中 \(k= m - h + m \lfloor \frac{h-1}{m} \rfloor\)。预测会自动将季节性成分预测添加到 ARIMA 预测中。

[12]:

from statsmodels.tsa.arima.model import ARIMA

from statsmodels.tsa.forecasting.stl import STLForecast

elec_equip.index.freq = elec_equip.index.inferred_freq

stlf = STLForecast(elec_equip, ARIMA, model_kwargs=dict(order=(1, 1, 0), trend="t"))

stlf_res = stlf.fit()

forecast = stlf_res.forecast(24)

plt.plot(elec_equip)

plt.plot(forecast)

plt.show()

summary 包含有关时间序列模型和 STL 分解的信息。

[13]:

print(stlf_res.summary())

STL Decomposition and SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 257

Model: ARIMA(1, 1, 0) Log Likelihood -522.434

Date: Thu, 03 Oct 2024 AIC 1050.868

Time: 15:45:57 BIC 1061.504

Sample: 01-01-1995 HQIC 1055.146

- 05-01-2016

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

x1 0.1171 0.118 0.995 0.320 -0.113 0.348

ar.L1 -0.0435 0.049 -0.880 0.379 -0.140 0.053

sigma2 3.4682 0.188 18.406 0.000 3.099 3.837

===================================================================================

Ljung-Box (L1) (Q): 0.01 Jarque-Bera (JB): 223.01

Prob(Q): 0.92 Prob(JB): 0.00

Heteroskedasticity (H): 0.33 Skew: -0.26

Prob(H) (two-sided): 0.00 Kurtosis: 7.54

STL Configuration

=================================================================================

Period: 12 Trend Length: 23

Seasonal: 7 Trend deg: 1

Seasonal deg: 1 Trend jump: 1

Seasonal jump: 1 Low pass: 13

Robust: False Low pass deg: 1

---------------------------------------------------------------------------------

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).