自回归移动平均 (ARMA):人工数据¶

[1]:

%matplotlib inline

[2]:

import numpy as np

import pandas as pd

from statsmodels.graphics.tsaplots import plot_predict

from statsmodels.tsa.arima_process import arma_generate_sample

from statsmodels.tsa.arima.model import ARIMA

np.random.seed(12345)

从 ARMA 过程生成一些数据

[3]:

arparams = np.array([0.75, -0.25])

maparams = np.array([0.65, 0.35])

arma_generate 函数的约定要求我们为 AR 和 MA 参数的零滞后指定 1,并且 AR 参数需要取反。

[4]:

arparams = np.r_[1, -arparams]

maparams = np.r_[1, maparams]

nobs = 250

y = arma_generate_sample(arparams, maparams, nobs)

现在,我们可以选择添加一些日期信息。在本例中,我们将使用 pandas 时间序列。

[5]:

dates = pd.date_range("1980-1-1", freq="M", periods=nobs)

y = pd.Series(y, index=dates)

arma_mod = ARIMA(y, order=(2, 0, 2), trend="n")

arma_res = arma_mod.fit()

/tmp/ipykernel_4466/3761908329.py:1: FutureWarning: 'M' is deprecated and will be removed in a future version, please use 'ME' instead.

dates = pd.date_range("1980-1-1", freq="M", periods=nobs)

[6]:

print(arma_res.summary())

SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 250

Model: ARIMA(2, 0, 2) Log Likelihood -353.445

Date: Thu, 03 Oct 2024 AIC 716.891

Time: 15:48:55 BIC 734.498

Sample: 01-31-1980 HQIC 723.977

- 10-31-2000

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.7905 0.142 5.566 0.000 0.512 1.069

ar.L2 -0.2314 0.124 -1.859 0.063 -0.475 0.013

ma.L1 0.7007 0.131 5.344 0.000 0.444 0.958

ma.L2 0.4061 0.097 4.177 0.000 0.216 0.597

sigma2 0.9801 0.093 10.514 0.000 0.797 1.163

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 0.29

Prob(Q): 0.96 Prob(JB): 0.86

Heteroskedasticity (H): 0.92 Skew: 0.02

Prob(H) (two-sided): 0.69 Kurtosis: 2.84

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

[7]:

y.tail()

[7]:

2000-06-30 0.173211

2000-07-31 -0.048325

2000-08-31 -0.415804

2000-09-30 0.338725

2000-10-31 0.360838

Freq: ME, dtype: float64

[8]:

import matplotlib.pyplot as plt

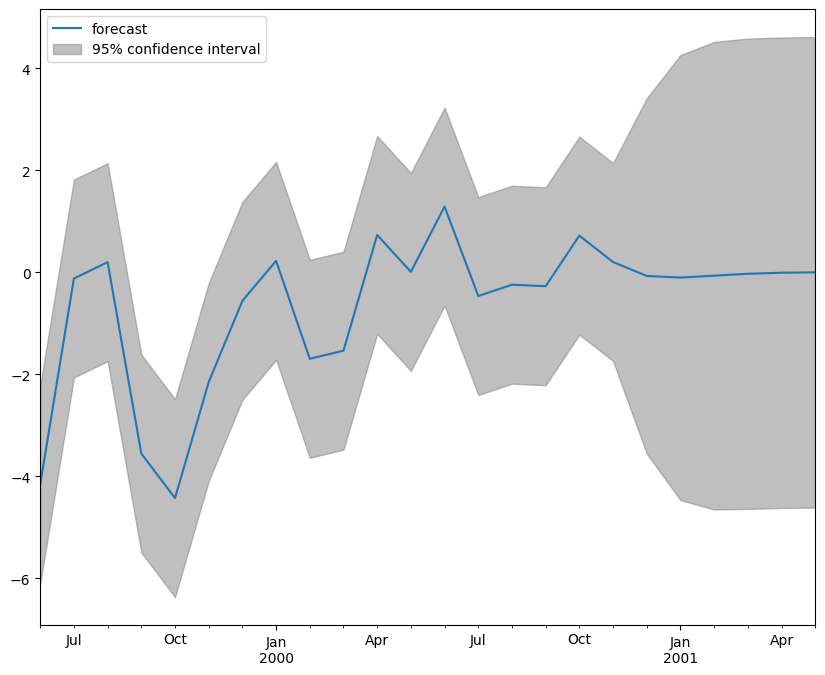

fig, ax = plt.subplots(figsize=(10, 8))

fig = plot_predict(arma_res, start="1999-06-30", end="2001-05-31", ax=ax)

legend = ax.legend(loc="upper left")

最后更新:2024 年 10 月 3 日